Highlights

- Market returns were driven by a combination of positive carry, narrowing spreads and lower base government bond yields.

- Short positions in credit were detractors on the portfolio.

- Contributors to the Fund included a position in Legends Hospitality 5% 2026 bonds, and from several new issues in Canadian and US high-yield markets at particularly attractive levels.

The Pender Alternative Absolute Return Fund finished August with a return of 0.21% bringing year to date return to 4.61%[1]. The Fund’s benchmark, the HFRI Credit Index (USD), returned 0.38% in August and 5.92% year-to-date.

A sharp decline in risk assets at the start of August was met with a strong risk-taking impulse that saw the high yield market put up one of its best months of 2024. Market returns were driven by a combination of positive carry, narrowing spreads and lower base government bond yields. The market did not make new lows for the year in spreads, and we believe that a traditionally very quiet second half of the month contributed significantly to the rally.

Portfolio Update

Despite the VIX spiking above 60 briefly on August 5, we found little in the way of attractive buying opportunities. Usually, it takes several weeks of volatility to generate outflows from credit which then drives forced selling and creates market opportunities. Credit held up much better than equities in early August, likely driven by the rally in government bonds and enthusiasm about a pivot from the Federal Reserve.

We suspect that the degree of enthusiasm for falling policy rates could prove to be excessive, as a lot of cuts are already priced in. We believe that the current pricing for rate cuts is unlikely to be followed through without significant weakening of economic fundamentals. The required economic weakness for rate curves to prove accurate would likely result in risk premiums being a fair bit higher than where they sit currently.

While short positions in credit were the biggest drag on the portfolio in August, the Fund benefitted from several positive events. Our position in Legends Hospitality 5% 2026 bond was called in connection with the closing of the company’s merger with ASM Global, resulting in about a 2% capital gain from purchases as recently as July. The Fund participated in several new issues in Canadian and US high yield markets including some first-time issuers that came at particularly attractive levels, helping to generate positive performance for the Fund.

The Fund’s overall positioning was not significantly changed in August as we recycled capital out of expensive positions in secondary markets into relatively more attractively priced new issues. The Fund also put cash to work in our Current Income strategy to offset T-bill maturities and called bonds. The purpose of our Current Income strategy is to generate attractive positive carry with low correlation t o broad markets.

“The concept of “goldilocks” or economic fundaments that are “just right” tends not to hold historically”

Market Update:

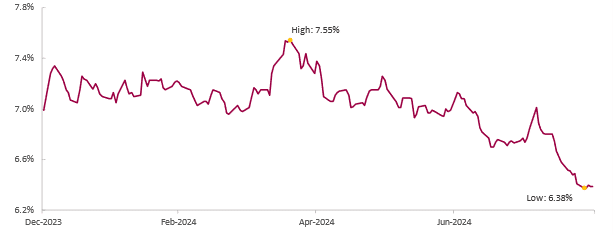

Spreads continue to look expensive by any historic metric. With the re-pricing of government curves, all-in yields now offer significantly less value than they did earlier in the year. While spreads have been expensive relative to historic levels all year, a reasonable counter argument in recent months was that all-in yields were still relatively attractive. With rates repriced lower, we believe this argument is increasingly difficult to make. The BB-B segment of the US high yield market which excludes the bottom 12% of the market, bottomed at a yield of 6.38% to worst on August 26, more than 100bp below April’s peak.

ICE BofA BB-B US High Yield Index – Yield to Worst %

Source: Bloomberg/ICE BofA

There is usually a negative correlation between government bond yields and spreads, as all-in yields attract buyers with absolute return targets, causing spreads to compress as base rates rise. Also, generally macro developments which are positive for treasuries are often negative for risk assets and risk premiums. This has not been the case recently as the market appears to believe that weaker economic data is positive for risk assets because it creates the ability for the Federal Reserve to lower rates. The concept of “goldilocks” or economic fundaments that are “just right” tends not to hold historically.

In our view, at a macro level something must give. Either economic conditions will prove to be weak enough to bring about dramatic easing that has already been priced in or the economy is relatively stronger and expectations for central bank policy accommodation are excessive. The market appears to want to have it both ways, enjoying the benefits of a dramatic policy response while pricing in strong earnings growth and low risk premia.

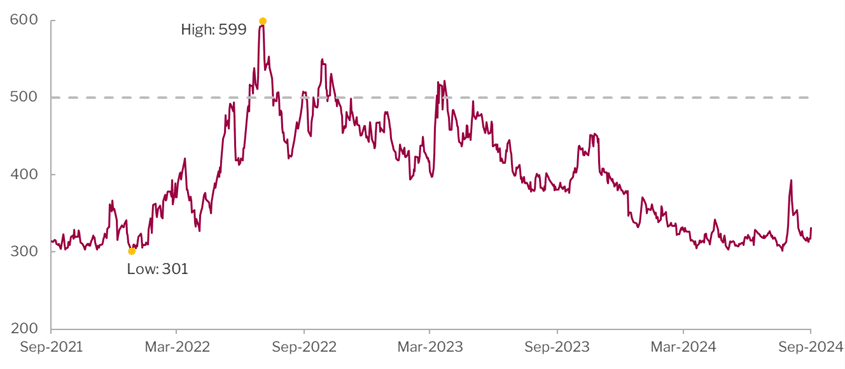

We have tilted our hedges toward risk assets for a while, covering a significant portion of our interest rate hedge earlier this year. The bar for risk assets to reprice is significantly lower than a recession. In most of the past 10 years the high yield market has hit 500bp or higher in spread, and only one of these events was associated with a recession, which caused spreads to widen much further than 500bp. From a starting value of 317bp, we believe the skew to where the high yield market can go from here is clear.

ICE BofA US High Yield Index – Gov’t OAS bp

Source: Bloomberg/ICE BofA

ICE BofA US High Yield Index

Source: Bloomberg/ICE BofA

It is noticeable that 2024 so far is tied with 2021 as the lowest peak spread value since the Global Financial Crisis. We believe the market’s apathy for potential risk repricing bears a lot of resemblance to 2021. There clearly are differences between the two market environments. We thought that the easier trade three years ago was to be short duration rather than risk assets, while now the opposite is true. Even with the strong recovery into the end of August, the increased volatility in recent weeks argues to us that market drivers are shifting which should eventually lead to better opportunities.

Portfolio metrics:

The Fund finished August with long positions (excluding cash) of 137.3%. 42.8% of these positions are in our Current Income strategy, 88.6% in Relative Value and 5.9% in Event Driven positions. The Fund had a -54.0% short exposure that included -5.2% in government bonds, -33.5% in credit and -15.3% in equities. The Option Adjusted Duration was 0.94 years.

Excluding positions that trade at spreads of more than 500bp and positions that trade to call or maturity dates that are 2026 and earlier, Option Adjusted Duration declined to 0.69 years. The Fund’s current yield was 4.6% while yield to maturity was 6.3%

Justin Jacobsen, CFA

September 11, 2024

[1] All Pender performance data points are for Class F of the Fund unless otherwise stated. Other classes are available. Fees and performance may differ in those other classes. Standard Performance Information for the Fund may be found here: https://penderfund.com/solutions/