Dear Unitholders,

The Pender Alternative Absolute Return Fund finished February with a return of 0.9%, bringing year to date return to 0.7%[1].

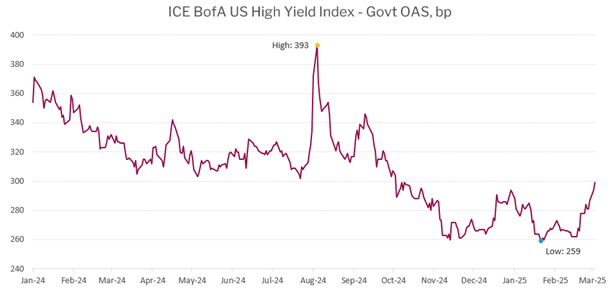

Credit markets produced positive returns in February as lower government bond yields offset widening credit spreads. The ICE BofA US High Yield Index returned 0.65% in February as spreads finished the month at 287bp Govt OAS, an increase of 19bp. The HFRI Credit Index, the Fund’s benchmark, generated a return of 0.9% in February.

Portfolio & Market Update

Although spreads widened modestly in February, we did not see meaningful opportunities to add value through trading. The positive absolute return for credit was indicative of a market where higher quality high yield bonds barely moved on dollar price. The hotter than expected US CPI report released on February 12 created opportunities for us to cover some individual high yield bond shorts and modestly increase the Fund’s duration.

We found opportunities to put cash to work in the Commercial Mortgage Backed Securities (CMBS) market in February. Driven by commentary from management on their Q4 results call late in the month we grew more confident in our thesis that Park Hotels & Resorts Inc. (NYSE: PK) is planning an early refinancing for the Hilton Hawaiian Village loan later this year. We added to our holdings based on higher conviction and believe that the yield to a likely call date later this year is around 10% for the F tranche of this mortgage.

We added a new position in a mortgage backed by the JW Marriott Phoenix Desert Ridge Resort & Spa, a 950-room property purchased in 2019 by Elliott Management Corp. for $602 million. As of September 30, 2024 Net Cash Flow generated by the property is 52% higher than the Underwriting Base Line, arguing that the property is likely worth closer to $900 million today. Our level of the CMBS is fully covered at about $332 million in asset value, or 37% loan to value based on our estimate. Much like the Hilton Hawaiian Village mortgage bond, one of the attractive features of the Desert Ridge bond is its discount to par. Our purchase price was $97.34 or 6.37% to maturity in September 2026. We believe that Elliott would likely be able to refinance the $400 million mortgage with a $600 million mortgage today, paying themselves a $200 million dividend which provides a strong incentive for an early refinancing, enhancing the return profile of our holding.

Despite a weak closing to the month, risk assets have been remarkably resilient in 2025. Both the Nasdaq 100 and S&P 500 hit all-time highs in February, despite weakness in cyclical industries like autos, a disappointing earnings season from the Magnificent Seven companies, and the incoming trade war between the United States and its primary trading partners. To us, it looks like technical factors have been supporting the market in the face of deteriorating fundamentals. Eventually, fundamentals will determine asset prices. Nissan Motor Acceptance Corporation was downgraded by multiple rating agencies in February and moved from the Investment Grade to the High Yield market. Ford Motor Credit Company was moved to negative outlook at Standard and Poor’s in February, a one notch downgrade would cause them to move back to the high yield market, following an elevation to investment grade in late 2023. The Fund has a small net short exposure to the automotive sector.

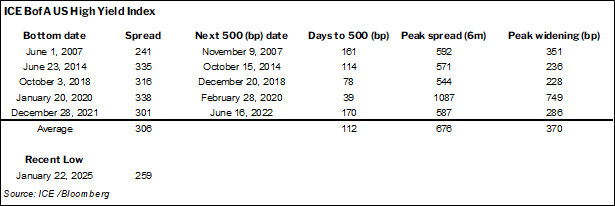

It is increasingly likely that the January low in high yield spreads will be a significant bottom. Once the market puts in a bottom in risk premiums there can often be a strong negative repricing event in the following six months, as widespread complacency is replaced with risk aversion.

While spreads have widened out since January, treasury yields have declined by a similar amount, resulting in limited price volatility and a scarce opportunity set for trading.

In early March with spreads just inside of 300bp, we believe that the market is still a long way from being cheap. If treasury yields stay close to current levels, we would need to see at least a 400bp high yield market before becoming constructive. If a spread widening event coincided with a significant treasury rally with lower treasury yields we would target closer to 500bp.

It appears to us that a regime shift is occurring in markets, as the reality of a trade war has upended previous assumptions about global trade which should result in higher risk premiums. Major shifts like the one occurring now take time to get priced into assets. The powerful rally in risk assets in 2023 and 2024 has created strong muscle memory for many market participants that every dip is a buying opportunity. This “buy the dip” impulse will take time to work through. We believe that patience and discipline are appropriate given current valuations, as the market is particularly vulnerable to any unexpected outside shocks.

Our focus for now is on higher quality and shorter duration positions, where liquidity is priced appropriately. More than fifteen percent of the Fund is invested in investment grade corporate bonds and commercial paper with maturities in March. We expect to re-invest only a portion of the proceeds as we expect that the value of liquidity is likely to increase in the next few months.

Portfolio Metrics

The Fund finished February with long positions of 121.8% (excluding cash and T-bills). 44.0% of these positions are in our Current Income strategy, 77.9% in Relative Value and 0.0% in Event Driven positions. The Fund had a -50.2% short exposure that included -3.8% in government bonds, -30.9% in credit and -15.5% in equities. The Option Adjusted Duration was 1.28 years.

Excluding positions that trade at spreads of more than 500bp and positions that trade to call or maturity dates that are 2027 and earlier, Option Adjusted Duration increased to 0.88 years.

The Fund’s current yield was 5.20% while yield to maturity was 6.07%

Justin Jacobsen, CFA

March 11, 2025

[1] All Pender performance data points are for Class F of the Fund unless otherwise stated. Other classes are available. Fees and performance may differ in those other classes. Standard Performance Information for the Fund may be found here: https://penderfund.com/solutions/