Dear Unitholders,

The Pender Alternative Absolute Return Fund finished March with a return of 1.2%, bringing year to date returns to 2.0%[1].

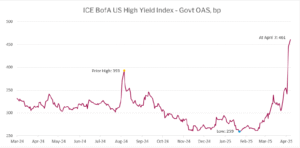

Risk assets performed poorly in March as euphoria surrounding Donald Trump’s inauguration was replaced by concern about the potential impact of tariffs on the global economy. The ICE BofA US High Yield Index returned -1.1% in March, driven by wider spreads, which finished the month at 355bp Option Adjusted Spread (OAS) compared to government bonds, 68bp wider on the month. The HFRI Credit Index, the Fund’s benchmark, returned -0.4% in March, bringing year to date returns to 1.4%.

Portfolio & Market Update

Over the past six weeks, the extreme levels of complacency in risk markets have been replaced by risk aversion in response to President Trump’s attempt to radically re-order global trade through tariffs.

We have highlighted in the past that once credit spreads bottom, significant repricing events often follow within the next six months. It is just over two months since a multi-decade bottom in high yield spreads and spreads have already surpassed the 10-year average. We expect that the full extent of this risk event will take weeks and months to play out and will likely be choppy once the initial shock is processed by the market.

Compared to market episodes in recent memory, like December 2018 and March 2020, we expect that it will be more difficult for the Federal Reserve to support the market given elevated inflation and the prospect of tariffs increasing inflation further. We expect volatility will likely be heightened for some time and for trading opportunities to increase as individual securities become more dislocated relative to peers and fundamentals.

In the initial aftermath of the “Liberation Day” announcement, we added to individual credit short positions, while also adding to long positions we believe were positioned to outperform the market. As a rule we generally do not discuss individual short positions, but one of our favorite themes in our short book are bonds that are rated BB by rating agencies which should be rated lower by virtue of business quality, scale and cyclicality. The BB rating category is the highest quality bucket of high yield, where there have historically been low losses from defaults. Some investment grade funds are permitted to hold BB rated bonds, which can offer an attractive yield pickup compared to the rest of their investing universe. This has been borne out by recent fallen angel downgrades (from BBB to BB) which saw very little selling from investment grade holders, while index influenced high yield investors were forced buyers, causing credit spreads to tighten on a downgrade to high yield. We suspect that some market participants are overly deferential to rating agencies and do not think as critically as they should about true fundamental credit quality when they see a BB rating.

After a weak but orderly first couple of days after Trump’s tariff announcement, forced selling became more evident in the second week of April. Disorderly market environments where buyers have the ability to dictate prices provide the foundation for good forward investment returns. While price adjustments likely still have some room to go, the market tone is the weakest we have seen since October 2023.

Previous assumptions about global trade have been upended, the second order effects of the upcoming changes are unclear and will only become evident over time.

Where to from here?

While markets are unlikely to move in a straight line, we believe that the path of least resistance for risk premiums remains higher. Subject to how the facts on the ground evolve, our best guess is that high yield spreads will peak in the 550-800bp range this year. We suspect that even in a recession spreads will not hit 1000bp this time given the relatively strong balance sheets of high yield issuers, higher Treasury yields and the potential for a Fed backstop for credit as occurred in 2020.

Source: Bloomberg / ICE

We expect to move cautiously to increase the Fund’s exposure to the market as yields and spreads increase. There will also be opportunities to sell into strength. The increase in volatility will allow us to ramp up the Fund’s trading activity which should help drive returns over time.

While the implications of a large re-set to global trade are understandably cause for concern, we believe that volatility and fear presents opportunities. If we successfully avoid defaults, we believe that as yields increase so will forward returns. It looks to us like 2025 will present more opportunities and dislocations than we saw in 2024.

Portfolio Metrics

The Fund finished March with long positions of 106.2% (excluding cash and T-bills). 27.3% of these positions are in our Current Income strategy, 78.9% in Relative Value and 0.0% in Event Driven positions. The Fund had a -49.5% short exposure that included -3.6% in government bonds, -32.0% in credit and -13.9% in equities. The Option Adjusted Duration was 1.26 years.

Excluding positions that trade at spreads of more than 500bp and positions that trade to call or maturity dates that are 2027 and earlier, Option Adjusted Duration declined to 0.66 years.

The Fund’s current yield was 5.43% while yield to maturity was 5.60%.

Justin Jacobsen, CFA

April 11, 2025

[1] All Pender performance data points are for Class F of the Fund unless otherwise stated. Other classes are available. Fees and performance may differ in those other classes. Standard Performance Information for the Fund may be found here: https://penderfund.com/solutions/