Fellow unit holders,

It has been a volatile first half of the year that has seen significant drawdowns in equity markets as valuations have reset in anticipation of weaker economic growth going forward. Investors have focused on the macro headwinds of rising interest rates as policy makers are intent on curbing demand to slow inflation.

Small cap and technology companies have been particularly affected against this backdrop with the Russell 2000 down -22.1%, the S&P/TSX Capped Information Technology sector down -39.7% and the tech-focused Nasdaq down -29.5% in the first half of the year. The TSX Small Cap was down -13.9% and has benefited from its higher weighting in energy and materials, which has been a rare bright spot in 2022. The Pender Small Cap Opportunities Fund was not immune to this drawdown and was down -9.8% in June and closed the first half of 2022 down -28.7%.

Inflation has been rising steadily this year, driven higher by strong consumption, supply chain bottle necks and energy prices. With this uncertainty at the macro level, we have remained focused on our research process and identifying fundamentally strong businesses. While these market episodes can be challenging to endure, it does create a significant breadth of opportunity for investors able to keep a long-term perspective and look past the murky macro environment. We have been adding to what we view as high quality small cap holdings that we believe can withstand a downturn in their industry and come out stronger.

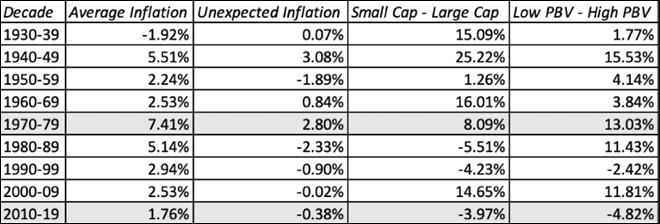

In a recent analysis of small cap company performance going back to the Great Depression[1], small caps were shown to outperform large caps by a healthy margin in periods where inflation was unexpectedly high. The chart below shows the performance of small cap companies in periods of inflation. This includes the 1960s and 1970s when small cap outperformance was over 16% and over 8% respectively.

Small Cap Performance in Inflationary Environments

There are advantages to being small. Smaller companies are more nimble and have cost structures that can adapt more quickly when the environment changes. They also have management teams who are closer to their customers, who can act decisively to incorporate necessary changes into their strategic planning and growth plans. Pricing power is also an important attribute as small companies can pass cost increases onto their customers to keep their margins intact. While we are not yet at 1970s levels of inflation, it is an interesting history lesson that highlights small companies and the results of their ability to adapt quickly when inflation surprises.

In recent months, our portfolio activity has been focused on adding high quality companies with strong unit economics, a long growth runway, competitive advantages and a history of solid execution. This continued in June and we added to holdings like Copperleaf Technologies Inc. (TSX: CPLF), Kinaxis Inc. (TSX: KXS) and Thinkific Labs Inc. (TSX: THNC) that fit this description. Magnet Forensics Inc. (TSX: MAGT) is another example that we talked about last month. It is a high-growth, profitable company with a solid recurring revenue base and customer retention. This is a company we have followed for many years. We believe it has a long growth runway and is attractively valued in the current market, which gave us this opportunity to own a high-quality compounder. The company has contributed positively to the Fund’s performance since it was added earlier in the second quarter.

In this challenging market we also had detractors with DREAM Unlimited Corp. (TSX: DRM) and Spartan Delta Corp. (TSX: SDE) among them during the month of June. While DREAM sold off in June, our research into its underlying fundamentals shows a different story as the business remained strong. The company posted positive results in their last quarter and continued to remain active in pursuing their goal to create shareholder value. The company launched and completed an initial public offering of Dream Residential REIT and created a +$1bn industrial development fund focused on the Greater Toronto Area. They also announced that recurring fees were up over the last year due to higher assets under management and fee-earning assets, increasing by $0.9bn from the end of 2021 to sit at about $10bn.

After contributing for most of the year, Spartan Delta saw its share price roll over in June. As recession fears mounted, oil prices fell in anticipation of slower economic growth in the coming quarters. Despite the pull back, the oil producer has benefited from high oil prices and is firing on all cylinders in our opinion. This was demonstrated by its Q1 results which highlighted significant free cash flow and production levels above expectations. The company is de-levering their balance sheet and, in our view, should hit their 0.5x leverage target by the end of the second quarter. With ample cash flow in this robust operating environment, capital allocation will be its key focus going forward. We continue to see the company as attractively valued relative to peers but have been reducing our weighting as our position has grown within the portfolio. We also fully exited our positions in Freshii Inc. (TSX: FRII) and LiveTiles Limited (ASX: LVT) in favour of what we believe are higher quality opportunities in this environment.

With the macro environment likely to remain murky in the back half of the year, growth has now been repriced and multiples have compressed. We are finding opportunities in fundamentally attractive businesses that we can buy at multiples we have not seen in years. We believe small caps as a group look attractive and have a well-documented history of outperforming coming out of bear markets. These opportunities do not present themselves often and we are busy, undertaking deep due diligence to identify those companies that have the brightest prospects for years to come.

Thank you for your continued support.

David Barr, CFA and Sharon Wang

July 13, 2022

[1] https://aswathdamodaran.blogspot.com/2022/05/a-follow-up-on-inflation-disparate.html