At Pender, we are often asked about our cash levels because it fluctuates over time depending on the individual Fund mandate and the opportunity set. One of the common misconceptions regarding some Pender mandates is that most outsiders think we have generated good risk-adjusted returns despite holding cash. However, we are of the view that good risk-adjusted returns have been achieved because of the opportunistic deployment of cash over the cycle. Without that cash, it would be impossible to deploy capital when individual stocks drop and “fat pitches” suddenly become available, or when the market enters one of its recurring corrections and great opportunities become more widespread.

Of note, our flagship Pender Value Fund (PVF) has averaged 20.7% cash on hand since its inception from July 2013 to October 2017. Cash levels have varied widely over that period, from a low of 3.5% in October 2016 to a high of 39.4% in May 2015. Cash as a percentage of the PVF at the end of October 2017 was above the historical average at 25.3%. These figures represent historical data points from the Pender Value Fund. Cash positions change over time and vary by mandate; however, below we explain Pender’s view of the role of cash as a strategic asset class within our investment process.

Deploying Cash: When and How

We are patient opportunists. We are perfectly willing to sit on cash and let it accumulate in the absence of compelling opportunities because we view cash as a call option with no expiration date. In our experience, when opportunities come along, they often don’t last very long, so it is important to have the means to act quickly. Generally we believe an investor should be as fully invested as possible, assuming one can find enough compelling risk-adjusted ideas to own a diversified portfolio. Otherwise, the rational default option is to hold cash.

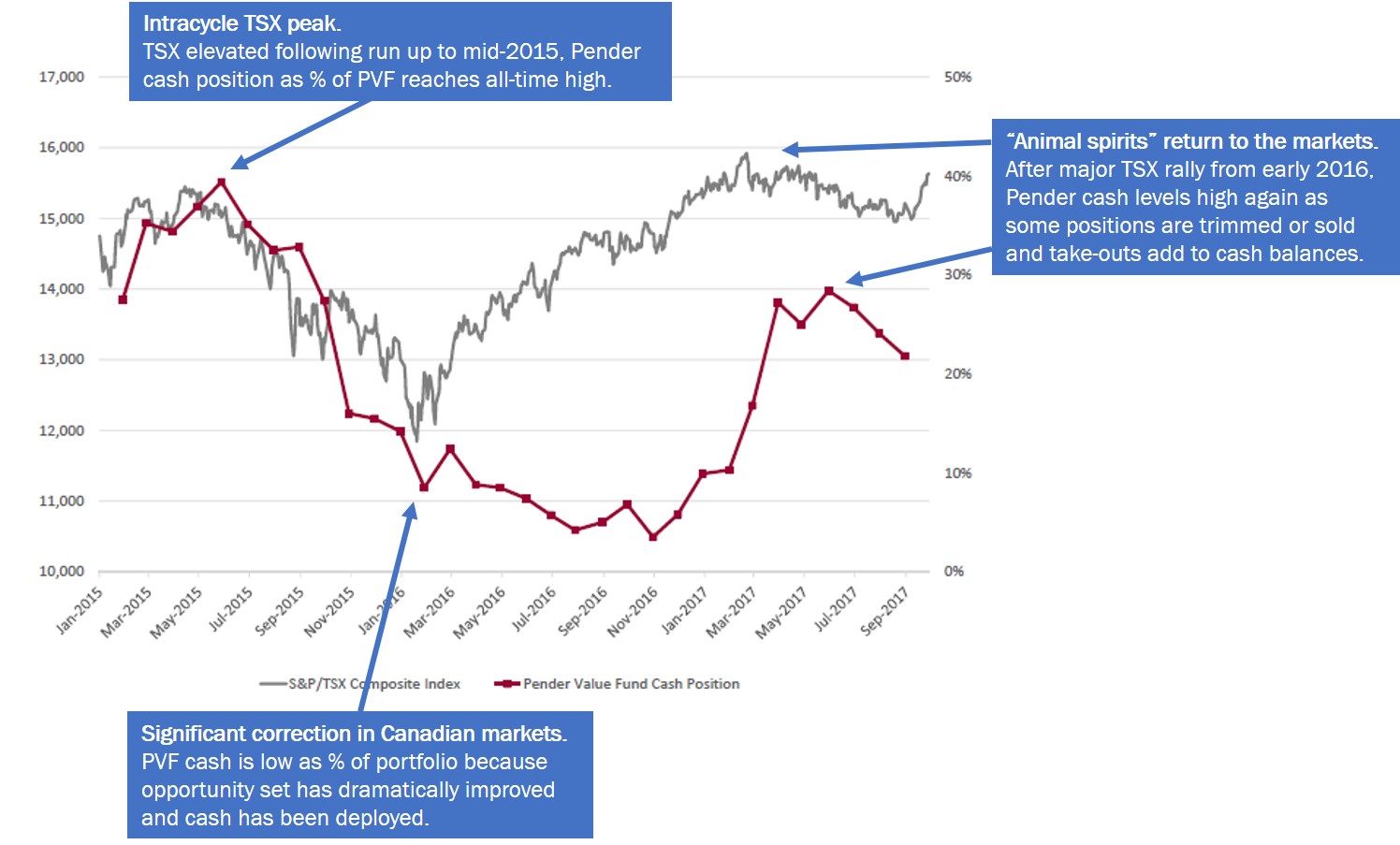

We believe the track record across a number of our mandates provides validation for this approach. The data shows that cash levels in the PVF vary widely depending on the market’s opportunity set. The chart below follows the fluctuating levels of cash as a percentage of the portfolio’s assets laid over the most recent cycle, and captures the Fund’s all-time high and low cash balance weightings.

TSX vs. PVF Cash Levels: Cash Increases During Market Run Ups; Is Deployed During Corrections

PVF’s all-time high in cash as a percentage of the assets occurred in May 2015, fairly near the TSX’s intracycle peak. Subsequently, the Canadian stock market sold off in the second half of 2015 and bottomed in early 2016. During the market correction, PVF’s cash reserve came in handy and was used to pick up bargains from our watchlist or increase weightings amongst the “best ideas” from our investment team. By mid-2016, the cash balance had fallen back into the low single digits as fears about a potential hard landing for China subsided and the market began climbing again.

With markets once again currently surpassing previous highs, we find ourselves selling more than we are buying, as during previous periods. Securities are trimmed or sold after our targets have been reached and cash is the default option as we await the next mispriced stock. This is particularly true amongst our lower quality “close-the-discount” ideas which require active trading strategies to generate returns. In addition, the cash uplift in the Fund can be partly attributed to recent take-outs.

Not a Market Call

Mathematically, all things being equal, when prices fall, prospective returns improve. Of course, the reverse is true as well. We believe changes to cash levels should simply reflect this recurring rhythm of the market when investing. Although PVF’s higher weighting in cash right now may look like a market call, in fact it’s a product of our process. The ebb and flow of a Fund’s cash levels should not be mistaken as an effort in market timing. We don’t believe anyone can consistently time the market. The stock market is a market of individual stocks, each of which has its own unique path, ups and downs that are not necessarily in sync with the broader markets. Rather than timing the market, we value individual businesses and securities that we believe we understand well enough to give us an investment edge, and then we act when stock prices are attractive relative to our fair value estimates.

During periods of market volatility, new ideas that have been tracked on our watchlist and those that fall in our circle of competence can be snapped up at a “discount” to our estimated fair value estimate. At the same time, we are frequently trading around our existing, high conviction holdings. Trading opportunistically around existing ideas tends to improve the odds of success because we are already very familiar with our holdings. Both watchlist and existing ideas hold a major advantage over other ideas during a selloff; we don’t need to jump start research efforts. We already have a qualified opinion whether the selloff was a buying opportunity or a time to sell and move on because the facts have materially changed.

Our investable universe is narrowed down to a reasonable size through our investment process. We have no opinion on the vast majority of stocks that are traded each day. The good news is that sound investing does not require one to know everything about all securities; an impossible task. But it requires an investor to thoughtfully assess the success factors for a handful of businesses better than the person (or more likely, an algorithm) on the other side of the trade.

Finally, we believe that large cash balances should not be held at all times. To do so serves as the financial equivalent of a security blanket, which acts as an anchor on compounding wealth over time. Maintaining high cash levels within relatively tight bands through all periods, without aggressively deploying it when compelling ideas arise, is not an optimal investment strategy, in our view.

Summary

Every position we hold is managed according to a unique investment thesis, developed out of the bottom-up, fundamental analysis of that security. The holding is actively managed according to that thesis, consequently if the stock reaches our target value, we find something better, or the facts change, our sell discipline guides us to trim or sell. We feel no pressure to be fully invested. We are patient opportunists. We are comfortable sitting on cash until the next attractive opportunity in something we understand comes around. The PVF’s track record shows that returns have been enhanced because of the strategic deployment of cash as an asset class.