Manager’s Quarterly Commentary – David Barr – Q3 2018

Fellow Unitholders,

I started drafting this commentary soon after quarter end, but then we were immediately presented with some interesting volatility in equity markets, so I put my pen down and went bargain hunting. Now, as I get back to writing this update, I can include what we’ve been doing recently.

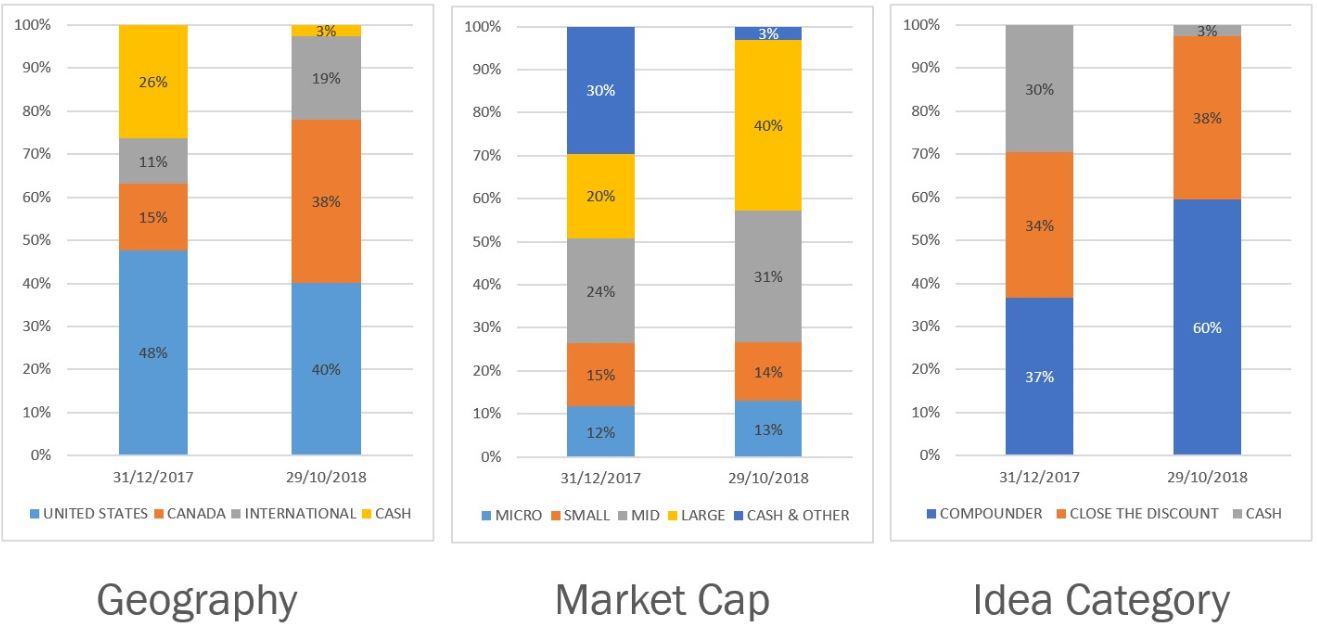

From our perspective, volatility and the underperformance in certain markets year-to-date has allowed us to deploy cash. The volatility has provided us with a lot of opportunities to shift the exposure of the portfolio. As of October 29, the Pender Value Fund was positioned as follows, compared to the end of 2017:

In this commentary we will discuss how the portfolio has changed and where we are seeing opportunities.

The rest of the world is selling Canada…

…so we are buying it. Low oil and other commodity prices, uncertainty in global trade and fears about Canadian housing have all been key reasons that Canadian markets have effectively gone nowhere for the past two years. This has created the opportunity for us to increase our Canadian exposure from 13% at the beginning of the year to 38% at September 30 in the Pender Value Fund. We have been able to deploy capital into our historical Canadian small and microcap universe (more on this later), but we have also been active in the midcap space and in the energy sector, thanks to the contributions of Amar Pandya who joined us over a year ago to focus on these areas.

Déjà vu

In 2015 we started to deploy cash into US listed companies. As small and mid cap stocks became cheaper we were able to buy companies we liked at an attractive price. But as is usually the case, momentum continued to work against us and a lot of these stocks became even cheaper. We’re not market timers. We’re not going to time investments to hit the bottom, so we focus on paying the right price. Similarly, in Canada, as we rotated back into Canada, momentum acted against us and while our performance has been dragged down by our Canadian universe year to date, we remain comfortable in the long term because we own businesses we like and understand, at what we believe is an attractive price.

Small and microcap Canada has gone to pot

If you picked up a national newspaper in the last couple of weeks, you will probably have noticed a substantial part of the business section was dedicated to the impending legalization date (now passed) of cannabis in Canada. The excitement about being a potential global leader in this “new” industry has resulted in over $10.5 billion being raised to finance various stage business plans. That’s a lot of money. The lack of interest we are seeing in micro and small cap names in our universe is directly related to this. The capital base that traditionally invests in this market has joined the massive “I want to get rich quick party”, aka the cannabis trade. To quote a musician one of my best friends believes is the greatest of all time, “We’re going to party like its 1999”. We just hope the hangover is not as bad.

US small and mid cap

This part of the market has been very interesting this year to say the least. One aspect that is very attractive to us is the volatility we witness. As a refresher for first time readers, for us, volatility is a wonderful tool that “Mr. Market” provides so that we can buy businesses we know well at a price below what we believe they are worth, before trimming or selling them when they become priced at a premium to their value. The first half of the year drove strong performance in the Fund and a lot was from this exposure. This came off a bit in Q3 and then October hit. The Russell 2000 was down 9% in early October and we experienced some of this in our portfolios. During this time, we saw several names in our universe fall around 50% from their 52-week highs. That’s a buying opportunity and that’s what we did.

A rotation to quality

Finally, when the market experiences volatility it gives us a chance to make switches within portfolios and to increase the quality of our portfolios. For example, we have been able to increase the weighting in businesses we view as compounders to 60% of the Pender Value Fund portfolio.

The future?

Well, we truly have no idea what is going to happen over the next few months. Momentum has turned negative and this could continue to drive markets down. Investor sentiment indicators, like the CNN fear and greed index, keep on bouncing off the “extreme fear” indicator. It would not be unexpected to see more downside in this type of environment. But we are not market timers. What we do know is that as prices decline, risk is reduced and future prospects improve, all things being equal. The Pender Value Fund today is at historical lows in cash, historical highs in allocation to compounders and the margin of safety, as we measure it, is very attractive today.

David Barr

November 5, 2018

For full standard performance information, please visit: http://www.penderfund.com/funds/