Manager’s Quarterly Commentary – Felix Narhi – Q4 2014

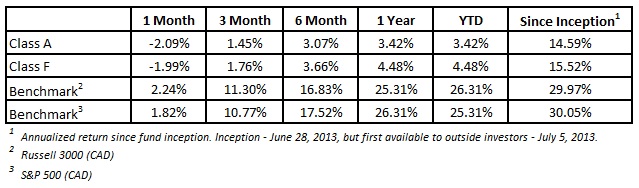

Class A units were up 1.45% during the quarter and were valued at C$12.27 at December 31, 2014. The Fund ended the year with 22 holdings and a cash weighting of 4.4%. During the quarter we sold our holdings in Vitamin Shoppe (VSI), Varian Medical Systems (VAR) and Liquidity Services (LQDT). We initiated stakes in Posco (PKX) and Altisource Portfolio Solutions (ASPS).

2014 in Review

Although we don’t take short-term results overly seriously, it is time to reflect on what worked and what didn’t work during the year. The Fund had a promising start during the first quarter of 2014 – a continuation from 2013, but faced headwinds for the balance of the year:

- US small-to-mid cap stocks posted one of their worst relative performances compared to large-to-mega caps since the late 1990s. The Fund’s heavy leaning towards US small-to-mid cap stocks was a meaningful headwind.

- A number of our largest holdings such as Syntel (SYNT) and Panera Bread (PNRA) increased in value and made notable progress during the year, but their stocks did not reflect this and provided mediocre returns in 2014, like many small cap stocks. Syntel continued to grow at a healthy clip while building up its IT staffing levels in anticipation of new contract wins over the next few years. In the most recently reported quarter (Q3), Panera posted its best quarterly transaction growth since Q1 2012 thanks to its customer experience enhancing initiatives (Panera 2.0) which we anticipate will continue to build momentum as they roll it out across the entire bakery-café chain. Both businesses have long histories of compounding their value at a strong double-digit pace and are currently trading at the lower end of their historical valuation ranges. We remain optimistic that the pent up value that was built last year should be unleashed in 2015 and beyond.

- The Fund’s positive contributors like Solarwinds (SWI), Brookfield Asset Management (BAM/A), Broadcom (BRCM) and Strayer Education (STRA) were largely offset by the Fund’s decliners like Leucadia (LUK).

- The Fund had a few stock specific impairments which impacted performance, most notably Liquidity Services (LQDT). We sold Liquidity Services at the end of the year after our investment thesis eroded because of the loss of Walmart as a major retail client, which followed an earlier contract termination by the US Department of Defense. Despite the company’s early success making inroads in the surplus assets industry, business risk was greater than we estimated – the company’s services were far less sticky with its customers than we had believed and the viability of the business model now looks questionable.

In 2014, the large-cap driven S&P500 went from strength-to-strength and is now trading near decade high valuations. The narrative on the American economy has almost completed a 180 degree turn from 5 or 6 years ago. The US economy is now widely considered one of the strongest major economies in the world and the greenback continues to strengthen relative to most other major currencies. Unfortunately, this favourable outlook is increasingly reflected in rising valuations in the US markets. US stocks are no longer broadly cheap which means that investors need to be more selective to find good value. We actively seek to avoid valuation risk because it is one of the main contributors of subpar long term returns. A year ago we believed valuation risk for the S&P500 was becoming elevated which implied that prospective returns would likely face headwinds, yet the large cap stocks continued to power upward. Today, valuation levels are even higher so, from our perspective, valuation risk has only increased as a result. Whenever valuations become elevated, we think it is prudent to look elsewhere for value and remain patient for the outlook and investor sentiment to change. We attempt to stack the odds in our favour by owning individual stocks trading at low valuations relative to our estimate of their intrinsic value. So if we are roughly right about our assessment, we can benefit from mean reversion as a tailwind rather than a headwind.

Some thoughts on finding value in the US markets

- While the broad US indices may not be necessarily cheap, there are always individual stocks in a market as deep and diverse as the US that are attractively priced because they are underappreciated, underfollowed or misunderstood.

- The fact that small cap US stocks, as represented by the Russell 2000, underperformed larger cap stocks in the S&P500 by the widest margin since the late 1990s is notable to us as contrarian investors. This implies that there should be better relative value available in small-to-mid caps today than a year ago.

- In addition, small US companies tend to be more leveraged to the strengthening US economy compared to the larger S&P500 companies, which tend to have more global exposure to challenged economies and weaker currencies.

The Fund’s “All Cap” mandate allows it to focus its holdings in any area of the market we can find the best value. Today, we continue to believe the best absolute and relative value, which will drive future returns, can be found in the small-to-medium cap universe and among individual names where pessimism has driven stock prices to low levels.

By weight, about 90% of the Fund’s holdings are listed outside of the S&P500. In contrast to the S&P500, the majority of the Fund’s holdings are trading below their historic average valuations and we believe many also have better underlying economics and medium-term growth prospects than the typical large American firm. According to our analysis, most of our holdings increased their intrinsic value and/or deepened their “moats” over the past year which we believe will show up in share price appreciation over time.

Please do not hesitate to contact myself, should you have questions or comments you wish to share with us.

Felix Narhi, CFA, February 4, 2015

Standard Performance Information (December 31, 2014)

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the simplified prospectus before investing. The indicated rates of return are the historical annual compounded total returns including changes in net asset value and assume reinvestment of all distributions and are net of all management and administrative fees, but do not take into account sales, redemption or optional charges or income taxes payable by any security holder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. This communication is intended for information purposes only and does not constitute an offer to buy or sell our products or services nor is it intended as investment and/or financial advice on any subject matter and is provided for your information only. Every effort has been made to ensure the accuracy of its contents. Certain of the statements made may contain forward-looking statements, which involve known and unknown risk, uncertainties and other factors which may cause the actual results, performance or achievements of the Company, or industry results, to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements.