It’s the height of summer and some of you may be taking road trip vacations. In a recent Forbes Wheels survey, 37% of electric vehicle (EV) owners reported either deferring a trip, changing an itinerary, or feeling anxiety during regular driving because of range anxiety, the fear of getting stranded somewhere because of a low car battery.

EV owners are not the only ones feeling range anxiety these days; investors and consumers are feeling it, too. Aggressive tightening by central banks and rising inflation are front-page news and are, understandably, unnerving market watchers and everyday folk alike. The questions on everyone’s mind are: how high will inflation rise, how far and fast will central banks hike rates to control it, and what effect will this have on economic growth and a potential recession? In this article, I’ll attempt to unpack where we are today and what’s ahead. And, spoiler alert, there are reasons for optimism despite the current headlines.

It’s going to be a long, hot summer: inflation in the spotlight

Amid scorching heat waves in Italy and Portugal, economic data in Canada and the U.S. also point to rising inflation numbers. “The Canadian economy is overheated,” Tiff Macklem, Governor of the Bank of Canada, said in a recent interview in The Globe and Mail. “Demand needs to slow so supply can catch up and price pressures ease.” This statement came on the heels of the Bank of Canada’s (BOC) announcement on July 13th of a 100-bp rise in the benchmark rate, the most aggressive hike since 1998. It was a larger move than had been expected and it puts Canada ahead of the G7 pack in terms of monetary policy. The BOC is forecasting inflation to average 7.2% this year before dropping to 4.6% in 2023; it expects to return to the 2% target by end of 2024. Inflation numbers in the U.S. remain elevated at 9.1% for June, a four-decade high. Like its Canadian counterpart, the Federal Reserve is expected to front-load rate increases with another 75-bp rise or higher which is rattling markets.

Rising inflation and aggressive tightening by central banks are hitting Canadian consumers’ pocketbooks hard. For example, for more than a decade, homeowners have benefitted from ultra-low rates. One outcome of this has been real estate bubbles in many parts of the country. Since the start of COVID, house prices in Canada have risen 26%. Since 2000, the average price of a home has tripled. Increasing home values have certainly made Canadians feel richer but, according to The Economist, they have also pushed average household debt levels to 185% of disposable income. Rising rates are cooling off this red-hot sector as Canadians watch their total net-worth decline. The number of home resales dropped 41% in June and prices have fallen 10% from their March peak to June, in Toronto, the country’s largest market.

Are we seeing peak inflation?

Yet, despite what we’re experiencing at the grocery store check-out, the barbershop, and on the links, prices are falling elsewhere pointing the way to a moderation of inflation. In an immediate response to the war in Ukraine, prices for raw materials like crude oil, copper, as well as corn and soyabean prices soared (cue central bank tightening). But there are signs everywhere that the tide is finally turning as recent prices for lumber, hot rolled steel, copper, oil, and cotton are all showing price weakness.

There are other signs that inflation may already have peaked. The Fed’s preferred measure of inflation—the Core Personal Consumption Expenditures Index (PCE), was down to 4.7% in May, still on the rise, but the third straight deceleration from the February peak. The US economy contracted again in the second quarter. Tariff relief is also in sight as Biden is close to rolling back Chinese tariffs.

Signs of Capitulation: Stocks Trading Underwater

Percent of companies trading below cash and short term investments

Why a recession may be shallow and mild

Google searches for “recession” are soaring as inflation worry gives way to anxiety about a possible recession brought on by aggressive tightening from central banks. Rising rates reduce demand for everything from raw materials to consumer goods and services leading to slowing economic growth. Everyone hopes for the best-case scenario of a mild economic downturn where inflation is under control and interest rates have not risen too high—albeit this is a tricky maneuver for central banks.

However, it seems a shallower recession is not out of the question as indicated by several factors including the important fact that high inflation is not entrenched and therefore should be easier to manage, robust employment, consumer resilience due to increased savings during the pandemic, a strong banking sector, and sustainable business profits. Only time will tell how the economy responds to the lively pace and magnitude of rate hikes.

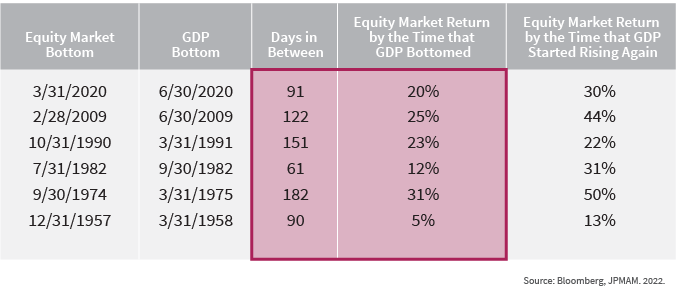

This is a good interlude to look back at previous recessions. During the past 30 years, the U.S. has had four of them: COVID in 2020, “The Great Recession” in 2007, the Dot-Com Recession in 2001, and the Gulf War Recession in 1990. The average recession lasts just under one year (around 11 months).

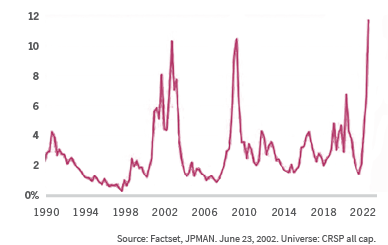

If we look at the relationship between the Consumer Sentiment Index and the subsequent 12-month return of the S&P 500, of 8 consumer sentiment troughs, the average return was 24.9% in the S&P 500. Historically, consumer sentiment seems to be a reliable predictor of robust stock market returns. The stock market is a leading indicator; on average stocks bottom 3-6 months before the economy does.

The good news, for long-term investors, is valuation risk is much lower today. A high percentage of stocks are trading below their cash levels. This could be a sign of capitulations, similar to 2003, and 2009. In addition, multiples in technology stocks, particularly those in SaaS are near all-time lows.

Waiting for Godot: The Opportunity Cost of Waiting for Economic Recovery Before Investing

There’s a silver lining

Although the headlines are portending much doom and gloom, it’s important to practice what Howard Marks calls “second-level thinking” which necessitates going beyond the headlines. As Marks’ says, “But the good news is that the prevalence of first-level thinkers increases the returns available to second-level thinkers. To consistently achieve superior investment returns, you must be one of them.” At Pender, we strive to practice second-level thinking and to delve beyond the headlines and to understand the complex interrelationships that can generate above-average investment returns.

Here are 5 reasons to be more optimistic:

- Inflation appears to be waning

- Record low consumer sentiment is a bullish signal

- Lower valuations imply higher future returns

- Markets will recover ahead of the general economy

- Pender strategies historically post the strongest returns following recessions

Those readers who were able to join us at the annual Pender Investment Conference in Toronto back in May were lucky enough to listen to our keynote speaker, Stephen Poloz, former Governor of the Bank of Canada, discuss his fascinating new book, The New Age of Uncertainty. In his keynote, Poloz discussed inflation, monetary policy and why increased volatility will remain the norm for the foreseeable future. If you missed it, view the video or read the 2-part excerpt from our interview with Poloz.

Stephen Poloz talks to Pender about his new book, The Next Age of Uncertainty – Part 1

In part one of two, Stephen Poloz, Special Advisor to Osler and former Governor of the Bank of Canada, talks about future economic volatility and the five tectonic forces driving it. Why title your book […]

The Pender Hot List: Summer Reading & Listening 2022

Pender’s ever-popular summer hot list is back! It’s packed with big ideas to challenge and inspire you on a range of topics