CIO’s Quarterly Commentary – Felix Narhi

“As to methods, there may be a million and then some, but principles are few. The man who grasps principles can successfully select his own methods.

The man who tries methods, ignoring principles, is sure to have trouble.” – Ralph Waldo Emerson

In this commentary we cover:

- Taking the capital out of capitalism – some implications for investors

- It’s different this time? It depends on the context

- The rise of FANG(MAN) and the value of mistakes lies in the lesson learned

Taking the Capital out of Capitalism

Never before in history have the largest global enterprises required so little tangible capital to generate enormous profits. These new digital business models are, in theory, infinitely scalable with very little incremental capital. For example, if Google, Facebook and Microsoft decided to return all their excess cash and non-core investments to shareholders via a special one-time distribution, the collective tangible capital left in their businesses would be modest. Yet, the lack of tangible assets from a traditional accounting viewpoint would have virtually no impact on their earnings power. Free cash flow would still be enormous and growing.

Financial reporting which was designed to approximate the previous tangible era has become less useful for investors today because the fundamental nature of capitalism has changed. Indeed, a recent Harvard Business Review article made a bold claim that, “accounting earnings are practically irrelevant for digital companies. Our current financial accounting model cannot capture the principle (sic) value creator for digital companies: increasing return to scale on intangible investment”. Directionally, the importance of intangible assets will only grow over time, relative to tangible assets. The essential raw material of more capital that was so critical for growth throughout the modern business era is becoming far less important.

The intangible benefits of technology-driven competitive advantage go far beyond the handful of ubiquitous online giants. Consider the restaurant business. This industry is very fragmented and most have historically been resistant to new technologies. Yet, Domino’s, the world’s largest pizza chain, often refers to itself as a “technology company” because it has become a key success factor for the company.

This pizzeria’s incredible turnaround started after Patrick Doyle became CEO in 2010 after some troubled years. He led efforts to completely overhaul its pizza recipe, root out poor franchisees and, most importantly, invest for the future and aggressively embrace technology to make ordering more efficient and customer friendly. The fundamental improvements of the business have been nothing short of stunning. Domino’s same-store sales, or sales from stores open at least one year, have risen in the U.S. market for 28 consecutive quarters at an average increase of 7.4% since 2010 which is well above all large peers. Today more than 60% of its orders come digitally and the firm is targeting 100%. The stock rose from below $9 per share in 2010 and has soared to more than $260 at the time of writing, an order of magnitude greater than its pizza chain peers. Domino’s is a wonderful example of the benefits of embracing technology as a competitive differentiator. Today, almost every successful restaurant operator is (or should be) trying to emulate some aspects of Domino’s extraordinary model. Source: tickertech.com

Source: tickertech.com

Closer to home, a few Pender mandates owned Panera and one still owns Starbucks, in part because these companies also make forward looking investments in technology as a competitive differentiator. We remain on the look out for more well run, traditional businesses which also see themselves more as “technology companies” in their space and are investing ahead of their peers. As we have seen, it can make a big difference and lead to a long runway of outperformance!

It’s Different this Time?

Legendary investor Sir John Templeton warned, “The four most dangerous words in investing are, it’s different this time,” and we wholeheartedly agree. We believe it is important to keep in mind that just about everything is cyclical. To wit, last year we wrote about cyclicality of the loonie and potential challenges to Canadian housing in the late innings of the cycle. Regrettably, some of these concerns are starting to bear fruit as interest rates have risen to multi-year highs over the past year. On the other hand, it is important to differentiate between swings within a cycle and structural changes. It is clear that the fundamental nature of capitalism and the drivers of successful business models are rapidly changing. It that context, perhaps it is different this time. For some historical context, consider when humanity moved from the agricultural era into the industrial era.

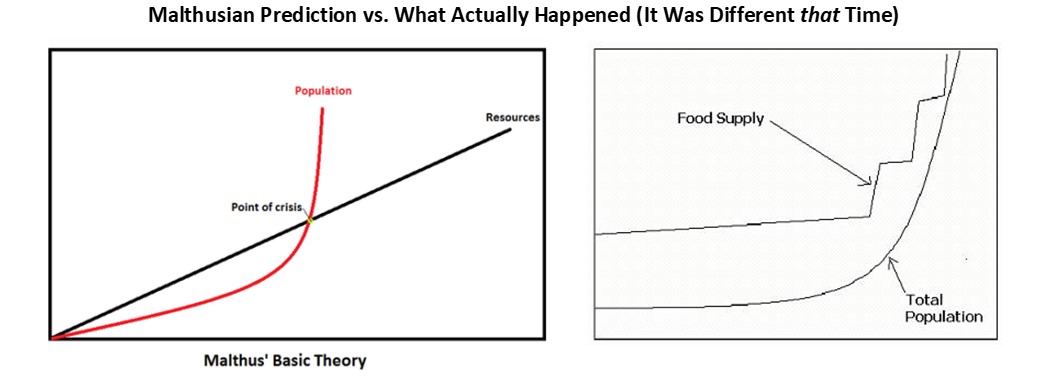

Born in England in 1766, Robert Malthus was one of the world’s first prominent economists. His life coincided with the beginning of the industrial revolution, but his world view was firmly shaped by the very harsh realities in agrarian society across many millennia. The central theme of Malthus’ work was that population growth would always overwhelm food supply growth, which would create perpetual states of hunger, disease and conflict. As such, Malthusians were raising the alarm and were sure a catastrophe as inevitable as global population began to soar during the dawning of the industrial era. If nothing changed, the Malthusians would have been right. Or at least, population growth would be generally restricted by available resources. But things did change.

The industrial age changed the fabric of society and coincided with new farming techniques and improved livestock breeding which lead to amplified food production. Later, mechanization created incredible food abundance which enabled the global population to grow rapidly unlike any other time in history. The Malthusians were wrong, because “that time it actually was different”. The old methods that worked so well in the past were no longer useful. The big fortunes of the industrial era were built by the Carnegie’s, Rockefeller’s and Ford’s of the world, not by the large U.S. agricultural land owners who had relied largely on slave labour during the agrarian era.

Source: https://www.youthdebates.org/t/malthus-vs-boserup/97538

Once again another huge structural shift is underway. The world is moving from the analog industrial era to the digital-driven world of the information age. Like the transition of the industrial revolution, this new world is harder to comprehend and requires new ways of thinking. Human nature has evolved over time to successfully navigate the world based on what is easy to understand. This is the world where, for example, the average person is 5 to 6 feet tall, the highest is about 8 feet and the shortest is about 2 feet. There are no exceptions to this distribution. In contrast, in the intangible digital-driven world, the tallest man could be 10,000 feet tall one day and the shortest might be negative 1,000 feet. This world is hard to conceptualize because it doesn’t make much sense in the world we live in. It is hard to overcome hardwiring that’s been optimized over thousands of years of human evolution. (for related reading, see Nassim Taleb’s concepts of Mediocristan & Extremistan in his classic book, The Black Swan).

Yet, we must adapt to this new world. The reality is that extreme outcomes are far more common in the intangible digital-driven world than in the tangible world. The rapid rise and domination of companies like Google and Facebook, driven by the winner-takes-all (or most) competitive dynamics of the digital world are unprecedented. This is largely due to the feedback loop of the network effect, or the positive effect that an additional user of a product or service has on the value of that product or service to other users. Due to the network effect, the larger the winners of many of these intangible businesses become, the faster they can grow (until they hit critical mass… nothing grows forever!). This dynamic is in sharp contrast to the industrial era, where growth rates generally slowed as businesses became larger, and it took much longer to reach critical mass, often measured in multi-decade timeframes. Rapid growth is far more feasible among large digital businesses than in older industrial industries because they are capital light and not constrained by time consuming needs like building factories or distribution centers and maintaining inventories that drive growth for these firms.

On the other hand, there is plenty of evidence that even the big winners, backed by powerful network effects, can still be fragile if they fail to reach true critical mass. Consider that in June 2006, social networking pioneer MySpace surpassed Google as the most visited website in the U.S.. By January 2018, MySpace was ranked 4,153 by total web traffic, and 1,657 in the U.S.. If social networking were an Olympic sport, Facebook would have taken the Gold medal whereas MySpace, winner of the Silver medal in social networking, might as well have been in last place. Quite often, the runners up are practically irrelevant in the digital world, whereas the second or third largest and even smaller businesses are still competitive in the industrial era. Winners tend to be singular leaders in their respective categories, so “paying up” for the leader makes sense in a world where there is only one real winner.

Similar to the Malthusians of the past, most people today have a hard time absorbing new mental models that are separate from those needed to thrive for most of human history. Not surprisingly then, investors tend to have a very difficult time conceptualizing exponential growth and are caught off guard when the world works differently than their pre-existing linear view.

In his thought provoking book Principles, famed investor Ray Dalio explained “Our biggest barriers to [being radically open minded] are the ego barrier and the blind spot barrier. Our ego barrier is our innate desire to be capable and having other recognize us as such. The blind spot barrier is the result of our seeing things through our own subjective lens; both barriers can prevent us from seeing how things really are. The most important anti-dote for them is radical open-mindedness…it is the ability to effectively explore different points of view and different possibilities without letting your ego or your blind spots get in the way.” As investors, to grow we need to be our own greatest critic and have the intellectual honesty to kill some of our best-loved ideas.

The rise of FANG(MAN) – aka FANG plus Microsoft, Apple, Nvidia

Regrettably, we have not owned a lot of the FANGMAN stocks (from the land of Extremistan) during their run up and which, collectively, have accounted for most of the returns from the large cap S&P500 index. We believe it is constructive to conduct “post mortems” on ideas as learning opportunities to improve the investment process. Mistakes come in two forms – errors of commission and errors of omission. Mistakes in the first category are visible and more obvious (why did we lose money on this idea?). The second category are invisible to the outside because they are excluded from returns but may actually be more important in the long run (why didn’t we buy this idea, what worked so well?)

As investors, we have been introspective about why we missed many of these massive winners, which continued to succeed as spectacular investments right under our noses, while as consumers we bought more of their products and used more and more of their services. Why did we miss them? Were they ego or blind spot related barriers? We believe there are four main reasons:

- As survivors of the dot com crash of 2000, we overlearned lessons from the past, repeating the self-congratulating, but inadequate mantra that “it is not different this time”.

- As value-focused investors, other ideas usually seemed “cheaper” at any given time.

- We tend to focus our attention on small to mid-sized companies. Companies that started off as large caps, like Facebook, and grew to become megacaps were generally off our radar screens.

- We were still overly influenced by our previous view of the world which had worked so well in the past, and did not fully appreciate that the very nature of value creation and capitalism was shifting.

In hindsight, it is humbling to have missed many of these companies because they do infact check off many of the investment principles of the Pender process. For starters, long time followers of Pender strategies know that we categorize all ideas into one of two camps (Compounders or Close-the-Discount) because capitalism follows the “80/20 rule” – a minority of stocks account for the vast majority of value creation in the stock market. The fact that Compounder-type FANGMAN stocks account for so much of the market’s total return does not offend us, because we view it as confirming a core principle of how the world actually works. The “80/20 distribution of capitalism” is clearly alive and well.

Second, many of these companies had predictive attributes which are particularly important when investing in Compounders. For instance, relative to benchmarks, Pender portfolios tend to skew toward founder run companies because they tend to outperform. In large cap land, most of big companies are older where the founders have departed the scene long ago. Yet, virtually all of these FANGMAN companies are either founder-led, or the founder had been involved until fairly recently. Also, many of these companies had “hidden assets” that essentially represented free options that were ultimately monetized which further fueled their run up. The presence of potentially valuable hidden assets is an important part of our valuation framework. Said differently, it is okay to buy a security at a “reasonable valuation” if it also comes with a bunch of free, but potentially very valuable, options (AWS at Amazon, YouTube at Google, WhatsApp at Facebook etc).

Third, we tend to skew our investments to technology companies, so most of these companies are within our circle of competence. Fourth, it is true that we tend to focus on small and mid cap because we believe the opportunity set is greater. Nevertheless, we are market cap agnostic in many Fund mandates, so the fact that these winners were large caps is no good excuse to miss them. Finally, we admit to being slow to embrace the new economic reality where the importance of intangible assets has surpassed the tangible for even the largest enterprise. Perhaps it was a lack of imagination, but it is always hard to envision scenarios that have never happened before. Yet, here we are. No need to imagine any longer. We just need to see the world for what it really is. We try not to be like the Malthusian, mid way through the industrial revolution, after seeing overwhelming evidence that our world view was mistaken, and still refuse to learn about the new models.

We are continually learning. We believe our principles remain sound, but we must overcome our ego and blind spot barriers so we can alter our methods to reflect how the real world works today and into the future. Over the last year, we have found a few compelling ideas that fit well into this new world. For example, although it is still early, TripAdvisor and Baidu are two good examples of larger cap investments that we may not have purchased as aggressively a few years ago. Not everything is about intangible digital businesses of course. Far from it. There is plenty of money to be made in seemingly mundane traditional businesses as our earlier Domino’s case study illustrates. However, it makes sense to keep in mind that even such sundry businesses can be turbocharged when management embraces technology as a competitive differentiator.

The value of a mistake lies in the lessons learned

We believe some investors still hold mental models that worked extremely well given world views in the industrial era. During long periods of continuity, it makes sense to use proven models and methods which have worked well, because they did a good job of approximating how the world worked. However, methods must change during periods of discontinuity, when new rules are written. Many investors are having trouble adapting to how the world actually works today because we are shifting to a world increasingly driven by intangible assets which require a different qualitative tool set to evaluate. Some are still using value investor Ben Graham’s valuation tools that worked in the 1940’s. They are hoping for cheap price-to-tangible book stocks to revert to the mean, even though the underlying business model may soon be obsolete. This is probably no longer the optimal strategy in a world that is increasingly “taking the capital out of capitalism” and where new business models quickly arise with winner-takes-most competitive dynamics.

Please do not hesitate to contact me, should you have questions or comments you wish to share with us.

Felix Narhi, June 19, 2018