Fellow unit holders,

It was a tough start to 2022, with January being one of the worst months ever for broad indices and our fund. The Pender Small Cap Opportunities Fund was down 7.8%[1] in January, while large and small-cap indices were also down: the S&P 500 Index (CAD) was down 4.7% and the Russell 2000 Index (CAD) was down 9.2%. In Canada, the S&P/TSX Composite Index only had a mild loss of 0.4% in January, mostly buoyed up by strong energy prices. In general, we are underexposed to the energy sector. The Fund has only two energy related holdings of which Spartan Delta Corp. (TSX: SDE) was a top contributor to the Fund in January.

We view the current drawdown as being mainly liquidity driven and the result of multiple contractions, as opposed to being company-specific fundamental deterioration. At this point in time, over 70% of companies in the S&P 500 Index have reported earnings, and 77% of those have beaten analyst estimates. The S&P 500 Index is reporting earnings growth of more than 30% for the fourth straight quarter and earnings growth of more than 45% for the full year[2]. If you just look at earnings growth, you would find it hard to believe that the S&P 500 Index had such a big drawdown.

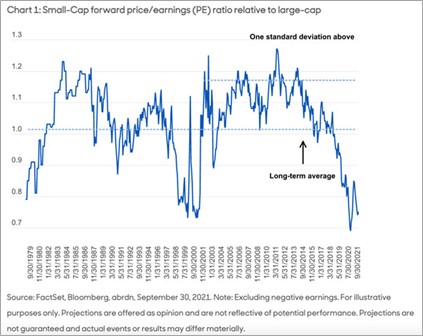

The small-cap universe was hit even harder, and many companies have not even reported earnings yet! The tide has been out for small-cap for the most part of 2021 and now rushing water starts to accelerate. When will the tide come back in? Short term, we do not know, but we are confident that rising tides will drive small-cap stocks for the next three to five years. We believe the current setup is extremely favourable for small-cap stocks. In our last commentary we talked about how valuations are disconnected from fundamentals for small-cap stocks, and valuations for small-cap stocks remain highly attractive in both relative and absolute aspects. The chart below shows that small-cap stocks are trading near their largest discount to large-cap stocks in the last twenty years.

Technology stocks also sold off in January. The Nasdaq Index (CAD) was down 8.6% and the TSX/S&P Capped Info Tech Index was down 12.0%. Many of our favourite ideas were negatively impacted in January including PAR Technology Corp. (NYSE: PAR), Sangoma Technologies Corporation (TSX: STC), Dye and Durham Limited (TSX: DND), and WeCommerce Holdings Ltd. (TSXV: WE). These are core holdings in the Pender Small Cap Opportunities Fund and we have high convictions that these businesses are fundamentally strong in the long term.

While we believe intrinsic value for these businesses has been increasing, share prices have been declining. As you would expect, we took this opportunity to add to some of our core holdings including PAR and Sangoma. We also initiated positions in three new names and completed the sale of four positions, including Farmers Edge Inc. (TSX: FDGE), where our thesis had broken down on unsatisfactory management execution.

We are never happy to see drawdowns in the Fund, but the flip side is that we become more opportunistic as our best ideas go on sale. We believe the current market environment has set up a very attractive long-term opportunity for our high-conviction holdings and is reminiscent of the early 2000’s and 2009-2010. As you can see from data below[3], in the subsequent one and three years following the dot.com bubble and the great financial recession in 2009, small-cap stocks made impressive returns. We believe now is a compelling time to initiate exposure to small-cap stocks.

David Barr, CFA and Sharon Wang

February 22, 2022

[1] All Pender performance data points are for Class F of the Fund. Other classes are available. Fees and performance may differ in those other classes.

[2] https://insight.factset.com/sp-500-earnings-season-update-february-11-2022

[3] https://www.institutionalinvestor.com/article/b1vzl8kqn0485p/Why-Now-Is-the-Time-to-Consider-Strategic-Small-Cap-Allocations