Protecting Capital | Why Pender?

Investing During Uncertain Times: Assessing the Trinity of Risk

Assessing the trinity of risk is a key pillar of Pender’s investment strategy at all times, but during a financial crisis, when the risks increase, it becomes more crucial than ever to double and triple check the level of catastrophic risk associated with every investment.

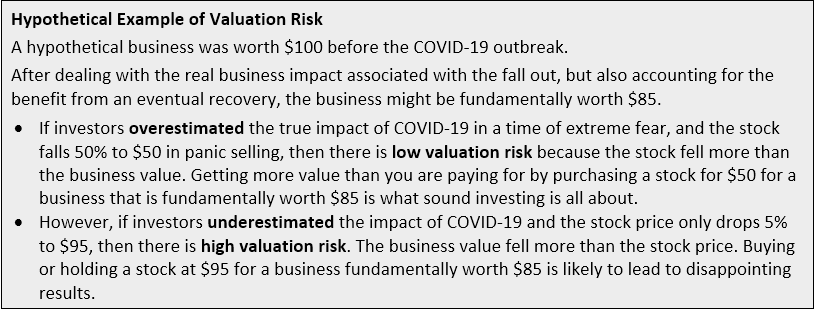

Valuation Risk

This is always important. Today, most stocks are well off their highs, so all things being equal, there is less “valuation risk” than just a few short months ago. But all things are not equal. Most companies will feel the negative impact from COVID-19, but a few will see benefits. How the market perceives the potential risk, relative to the long-term fundamental reality, is a very important consideration when investing. Stock prices can sway wildly from their fundamental values, particularly when extreme greed helps to create “bubbles” and extreme fear fosters panic during bear markets as we are seeing today.

Balance Sheet Risk

This is at the forefront of our analysis and we are reducing or eliminating weightings in companies that are over-levered relative to our assessment of their businesses risk. Surviving a market downturn is key. Debt reduces flexibility and can be potentially fatal for businesses with high business risk. A reasonable level of debt in normal times can become catastrophic when business activity comes to a halt.

Business Risk

The facts have changed for almost every business due to COVID-19. Some industries have been hit very hard over the short term like airlines, offline retailers, restaurants and the travel sector, but some businesses have seen a massive demand boost, such as online grocery delivery and work-from-home related firms like video conferencing solution providers. Some businesses are facing headwinds today but could experience booming demand in a post COVID-19 world – infrastructure firms and legal services are potential industries that come to mind. Remember that although most businesses have been hit hard right now, many will recovery eventually. For example, China was the first to experience fallout from COVID-19, but many businesses including restaurants have now reopened as the first steps are taken towards normalization. Of note, there is pent up demand as Chinese consumers start to emerge from months of being trapped at home in some cases, many excited to get out, get back to work, and ramp their consumption of goods and services back up. Some Chinese stocks are now trading near 52-week highs (for instance, we own shares in JD.com, “the Amazon of China”, in a few of our mandates). Still, it’s important to acknowledge some businesses will not survive the downturn or will be severely hit. It is important to assess business risk because it impacts the fundamental value of a business. If business risk is so high that the fundamental value is likely to be zero, no price is too low to sell.

The situation remains fluid, but we are focused on updating our thinking about potential risks and opportunities of existing holdings. Now is not the time to sell a sustainable business with a robust balance sheet that is very undervalued due to broad-based market fear that we believe will eventually pass. In addition, there is an entirely new opportunity set of ideas that did not exist a few months ago, many of which could see sharp rebounds in the recovery scenario in the future.

PenderFund and Felix Narhi

April 2, 2020

Investing During Uncertain Times: What is Pender Doing?

When the facts change, we change our minds The nature of most human activity is that the facts involved tend to change, but often not as abruptly, and rarely on such a wide scale as […]

Investing During Uncertain Times: Positioning for the Recovery

How the portfolio is positioned to capture potential gains We believe the world will be a very different place on the other side of the global health crisis and associated financial crisis. We know that […]

Four Potential Investment Strategies in a Stock Market Correction

Investors had largely ignored COVID-19 for over a month, but now emotions have started to get the better of cooler heads, and markets have reacted. Extreme fear has taken over. Unfortunately, emotional trading can quickly […]